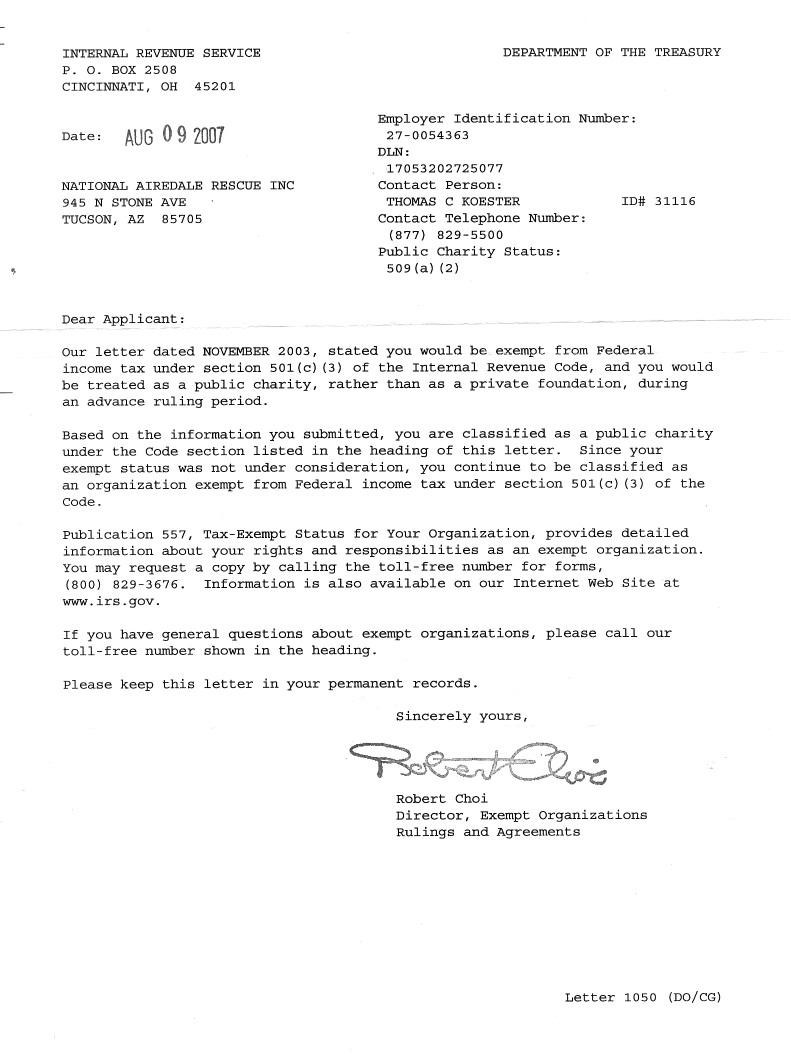

|

Based on information you supplied, and assuming your operations will be as stated in your application for recognition of exemption, we have determined you are exempt from federal income tax under section 501(a) of the Internal Revenue Code as an organization described in section 501(c) (3).

Because you are a newly created organization, we are not now making a final determination of your foundation status under section 509(a) of the Code. However, we have determined that you can reasonably expect to be a publicly supported organization described in sections 509(a) (2) .

Accordingly, during an advance ruling period you will be treated as a publicly supported organization, and not as a private foundation. This advance ruling period begins and ends on the dates shown above.

Within 90 days after the end of your advance ruling period, you must send us the information needed to determine whether you have met the requirements of the applicable support test during the advance ruling period. If you establish that you have been a publicly supported organization, we will classify you as a section 509(a) (1) or 509(a) (2) organization as long as you continue to meet the requirements of the applicable support test. If you do not meet the public support requirements during the advance ruling period, we will classify you as a private foundation for future periods. Also, if we classify you as a private foundation, we will treat you as a private foundation from your beginning date for purposes of section 507(d) and 4940.

Grantors and contributors may rely on our determination that you are not a private foundation until 90 days after the end of your advance ruling period. If you send us the required information within the 90 days, grantors and contributors may continue to rely on the advance determination until we make a final determination of your foundation status.

If we publish a notice in the Internal Revenue Bulletin stating that we will no longer treat you as a publicly supported organization, grantors and contributors may not rely on this determination after the date we publish the notice. In addition, if you lose your status as a publicly supported organization, and a grantor or contributor was responsible for, or was aware of, the act or failure to act, that resulted in your loss of such status, that person may not rely on this determination from the date of the act or failure to act. Also, if a grantor or contributor learned that we had given notice that you would be removed from classification as a publicly supported organization, then that person may not rely on this determination as of the date he or she acquired such knowledge.

If you change your sources of support, your purposes, character, or method of operation, please let us know so we can consider the effect of the change on your exempt status and foundation status. If you amend your organizational document or bylaws, please send us a copy of the amended document or bylaws. Also, let us know all changes in your name or address.

As of January 1, 1984, you are liable for social security taxes under the Federal Insurance Contributions Act on amounts of $100 or more you pay to each of your employees during a calendar year. You are not liable for the tax imposed under the Federal Unemployment Tax Act (FUTA).

Organizations that are not private foundations are not subject to the private foundation excise taxes under Chapter 42 of the Internal Revenue Code. However, you are not automatically exempt from other federal excise taxes. If you have any questions about excise, employment, or other federal taxes, please let us know.

Donors may deduct contributions to you as provided in section 170 of the Internal Revenue Code., Bequests, legacies, devises, transfers, or gifts to you or for your use are deductible for Federal estate and gift: tax purposes if they meet the applicable provisions of sections 2055, 2106, and 2522 of the Code.

Donors may deduct contributions to you only to the extent that their contributions are gifts, with no consideration received. Ticket purchases and similar payments in conjunction with fundraising events may not necessarily qualify as deductible contributions, depending on the circumstances. Revenue Ruling 67-246, published in Cumulative Bulletin 1967-2, on page 104, gives guidelines regarding when taxpayers may deduct payments for admission to, or other participation in, fundraising activities for charity.

You are not required to file Form 990, Return of Organization Exempt From Income Tax, if your gross receipts each year are normally $25,000 or less. If you receive a Form 990 package in the mail, simply attach the label provided, check the box in the heading to indicate that your annual gross receipts are normally $25,000 or less, and sign the return. Because you will be treated as a public charity for return filing purposes during your entire advance ruling period, you should file Form 990 for each year in your advance ruling period that you exceed the $25,000 filing threshhold even if your sources of support do not satisfy the public support test specified in the heading of this letter.

If a return is required, it must be filed by the 15th day of the fifth month after the end of your annual accounting period. A penalty of $20 a day is charged when a return is filed late, unless there is reasonable cause for the delay. However, the maximum penalty charged cannot exceed $10,000 or 5 percent of your gross receipts for the year, whichever is less. For organizations with gross receipts exceeding $1,000,000 in any year, the penalty is $100 per day per return, unless there is reasonable cause for the delay. The maximum penalty for an organization with gross receipts exceeding $1,000,000 shall not exceed $50,000. This penalty may also be charged if a return is not complete. So, please be sure your return is complete before you file it.

You are not required to file federal income tax returns unless you are subject to the tax on unrelated business income under section 511 of the Code. If you are subject to this tax, you must file an income tax return on Form 990-T, Exempt Organization Business Income Tax Return. In this letter we are not determining whether any of your present or proposed activities are unrelated trade or business as defined in section 513 of the Code.

You are required to make your annual information return, Form 990 or Form 990-EZ, available for public inspection for three years after the later of the due date of the return or the date the return is filed. You are also required to make available for public inspection your exemption application, any supporting documents, and your exemption letter. Copies of these documents are also required to be provided to any individual upon written or in person request without charge other than reasonable fees for copying and postage. You may fulfill this requirement by placing these documents on the Internet. Penalties may be imposed for ailure to comply with these requirements. Additional information is available in Publication 557, Tax-Exempt Status for Your Organization, or you may call our toll free number shown above.

You need an employer identification number even if you have no employees. If an employer identification number was not entered on your application, we will assign a number to you and advise you of it. Please use that number on all returns you file and in all correspondence with the Internal Revenue Service.

If we said in the heading of this letter that an addendum applies, the addendum enclosed is an integral part of this letter.

Because this letter could help us resolve any questions about your exempt status and foundation status, you should keep it in your permanent records.

If you have any questions, please contact the person whose name and telephone number are shown in the heading of this letter.

Sincerely yours,

(signed) Lois G. Lerner

Director, Exempt Organizations

Rulings and Agreements

Enclosure(s): Form 872-C

Letter 1045 (DO/CG)

|

{kind=link}